It is really surprising for me to see a bank run at this age. I always assumed that the banking sector is safe and solid. Thanks to the regulations in place after Lehman Brothers’ demise.

I believe by now, the current bank run and bank situation need no further explanation from me.

But I do notice the flaws in my investing process.

Emphasis on the numbers

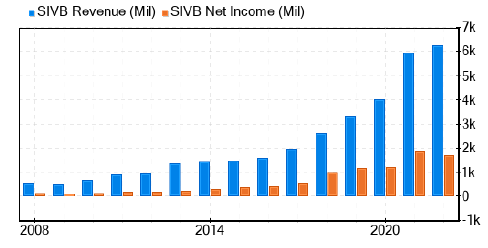

As a value investor, I checked the financial statements. As they reveal the company’s financial health.

I checked the trend of the company’s net profit, revenue, and other important information for the past few years, to check if the company is prospering.

This information depends on the past few years' financial statements. It is important for me, as I prefer to hold the company for many years.

If for the past few years, the company has been performing well, it MAY perform well for the next few years.

At the time of writing, a lot of information regarding SVB Financial Group (SIVB) and Silvergate has been purged.

But luckily I managed to find something.

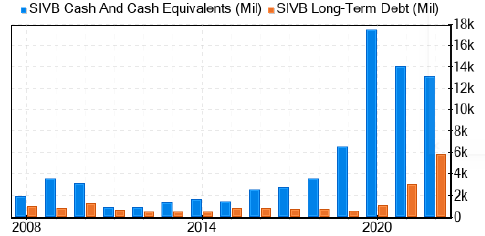

But it still gets assassinated by the bank run.

Therefore, using my method of just focusing on the numbers doesn’t help in filtering out a company from collapsing.

In this bank run, once the depositors have no faith in the bank, the bank will just fail and collapse. It's profitability and hard work in the past have no meaning.

In short, checking on the financial statement and looking at its trend does not help against the bank run.

What can help me improve my investment process?

Big Four gets the money

Based on this article, “https://seekingalpha.com/article/4587688-bank-stock-panic-5-attractive-buys-that-could-benefit”. The Big Four, JP Morgan, Bank of America, Citigroup, and Wells Fargo have been benefitting from this situation.

However, No bank can survive a bank run, no matter how big the bank is.

Yet, depositors still put their money with them.

Why?

Reputation has an effect (Economic Moat?)

I had a chat with my non-investment-savvy friend regarding this bank run. I have forgotten how the discussion went but somehow I did mention that if given a choice, which company will I invest in Singapore if I am given only 1 choice?

Without doubt and hesitation, I will pick DBS.

“Government mah” is my friend's remark on my choice.

His remark shows light on my above question regarding depositors going to Big Four.

DBS needs no introduction, but a brief background, DBS was set up to improve Singapore’s economic development by the Singapore Government.

Thanks to this history, and the Singapore Government’s reputation, Singaporeans have a lot of faith and trust in our Government to make things work.

I'm pretty sure he didn’t check how much net profit DBS has, and the amount of cash it has, and compared them with OCBC and UOB.

I am sure he didn’t do a series of due diligence to check if DBS is a prospering and good company.

Yet, we come to an agreement that DBS is a good company.

All he needs to know is that DBS is from the Singapore Government, it is safe. Short and Sweet.

This could be the case of the bank run and the Big Four’s unexpected benefits.

Thanks to their reputation and branding, they gained more deposits, allowing them to make more loans or investments.

Humble Pie to Eat

So I am wrong. Reputation and branding matter. Especially in times of faith and confidence are tested.

However… this leads to a new question…

How do I assess a company’s reputation?

Hmm…

Disclaimer: I do own Bank of America and OCBC Shares.

No comments:

Post a Comment